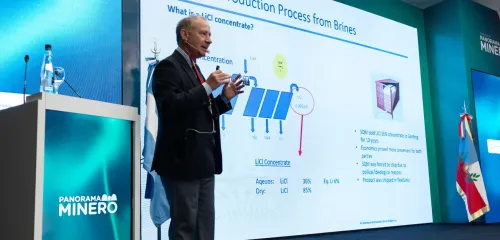

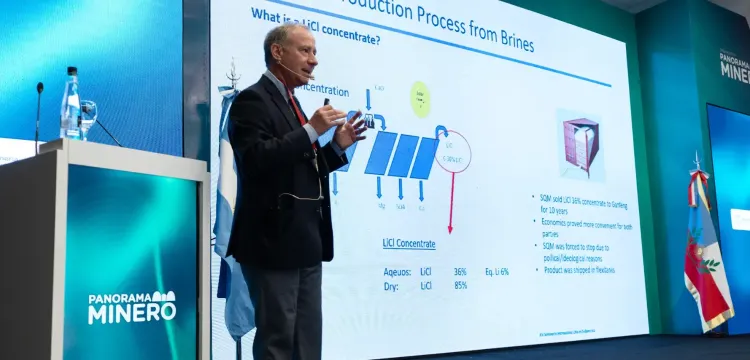

Despite strong global demand growth — projected to triple over the next decade — the lithium market is facing an oversupply scenario that has driven sustained downward pressure on international prices. Federico Gay, Principal Analyst at Benchmark Mineral Intelligence, reported that the market is currently producing around 150,000 tonnes more lithium than is being consumed, a gap that could keep prices low for at least the next two years.

By Panorama Minero

Gay delivered the opening presentation of the second day of the 14th Lithium in South America conference, organized by Panorama Minero since 2011 and this year bringing together some 950 participants in Catamarca. His remarks offered a clear assessment of supply-demand dynamics and the structural challenges shaping the market outlook.

He noted that industry sentiment is currently “mixed,” but emphasized the remarkable growth in demand over the last decade and the positive long-term trajectory. “Ten years ago, demand stood at 160,000 tonnes of lithium; today it is at 1.3 million. Over the next 10 years, demand is expected to reach 3.8 million tonnes,” he explained.

According to Gay, battery and energy storage demand is rising sharply, led by China (+30%), the European Union (+28%), and the United States (+8%), primarily driven by electric vehicle adoption. In 2025 alone, lithium demand will increase by 24% compared to last year, with 65% of that demand tied to EV production. “The compound annual growth rate is 15% — no other mineral shows that projection. However, there are clear signs that the lithium market remains immature,” he said.

Reviewing the last quarter, Gay stressed that there were no production losses and no major demand shifts; the determining factor for prices is supply. He noted that an additional 100,000 tonnes from Africa will enter the market this year, while global production will increase by 200,000 tonnes compared to 2024, pushing the balance further into oversupply.

“We are producing more lithium than we are consuming,” he summarized. Gay projected that this situation could last two to three years, possibly leading to production shutdowns or project delays. “It’s not what we want to hear, but this can improve,” he admitted, highlighting the current fragility of the market.

For Benchmark’s analyst, competitiveness will be critical. “It doesn’t matter if we have the best deposits or the highest grades. That helps, but the key is keeping costs low. That’s what makes us competitive globally,” he concluded, adding that most projects in Argentina and across the Lithium Triangle are aligned with this approach.